Bitcoin: The Next Savings “Rule of Thumb”

Three fundamental shifts at the macro, political, and geopolitical level are underway, making it likely that bitcoin is the next "rule of thumb" for savings.

A Brief History of Money & the Fiat Financial System

Sound money is a reliable store of value, a medium of exchange, and a unit of account. Over thousands of years, monies competed with each other, and eventually, humans settled on gold as the best money.

Through a free market selection process, humans settled on gold as the most desirable form of money, which became widely accepted and used in many civilizations due to best embodying the six critical properties of money: scarcity, divisibility, durability, portability, verifiability, and fungibility.

1. Scarcity: hard to produce and obtain.

2. Divisibility: can be easily divided into smaller units and grouped into larger units.

3. Durability: not perishable or easily destroyed.

4. Portability: easy to transport.

5. Verifiability: easy to verify that it is real.

6. Fungibility: all the same, interchangeable.

Of the traits listed above, the most important is scarcity. Money must be scarce to store value over time, which allows us to amass wealth and plan long-term.

This is beneficial not only for ourselves and our families but for civilization as a whole. If money is not scarce and the supply can be easily increased, someone will always find a way to increase the supply to his benefit, diluting the purchasing power of all others holding that money.

That should sound familiar because although our ancestors settled on the hardest form of money over thousands of years, today, we have fiat currencies, decreed by governments and backed by nothing.

Fiat currencies cost virtually nothing to produce. Thus, central banks and governments find reasons to increase the money supply for their benefit at our expense. The result of increasing units of fiat currency is the decrease in our purchasing power over time.

The rate at which new money is created directly impacts the rate at which our savings lose their value. As you can see in the chart below illustrating the United States’ money supply, there has been a constant increase over time, with an acceleration over this decade.

And as we have all experienced in the past three years, our dollars (or other fiat currencies) have been able to pay for less goods and services. Due to the money printing by these glorified counterfeiters, fiat currencies fail at storing value into the future.

Since 1971 when President Nixon abandoned the gold standard, there has been no constraint to increasing the supply of the dollar. The result of this has been an increase in the cost of living. Everything gets more expensive because fiat currencies become more and more worthless.

For a minority of the population, their earnings have kept up or surpassed the rate of inflation, affording them the ability to have savings; however, the majority have seen their wages increase far less than their cost of living. As a result, their quality of life has decreased, and more people are filled with despair, which explains many of the issues society faces today.

Rule of Thumb: How We Protect Against Inflation

We assume that if you are reading this newsletter, you are in the minority. You are fortunate enough to earn or have earned in excess of your expenses. You have been able to save money, likely due to a mixture of hard work, education, family support, and good luck. However, that is not enough.

We have sacrificed a substantial amount of time to earn money to support ourselves and our families, yet there is more work to do. Due to the nature of fiat currency described above; namely, that governments and central banks have a bad habit of legally counterfeiting more currency units, our savings do not hold their purchasing power into the future. Since the fiat thieves are constantly picking our pockets, we must invest those savings.

Rather than being able to earn money and save it to preserve our wealth, we have to become investors, which is almost another full-time job, or we have to pay someone we can trust to do that work for us.

Simply put, since the supply of fiat currencies is being expanded constantly and at increasing rates, we cannot save money. Saving has become complicated because it requires investing to preserve our purchasing power against inflation.

Because savings has become equated with investing and the investment landscape changes, the best way to save has gone through many iterations over the decades. There have been several "rules of thumb" for saving as the world has changed. A rule, meaning "a broadly accurate guide or principle, based on experience or practice rather than theory."

If your savings (investing) strategy does not change as the world does, then you can expect that your savings will end up losing the race against inflation.

As we reflect on our relationships, family, and friends and think about how personal finance has changed over the years, various "rules of thumb" for savings come to mind.

Generational Rules of Thumb

The Greatest Generation & The Silent Generation:

Largely saved with precious metals, savings accounts, certificates of deposits (CDs), and government bonds.

Depending on when they were born, they either experienced the gold standard in the early stages of their lives or were born in the years following the creation of the Federal Reserve.

Since gold was still part of the monetary system, there was a constraint on the number of new dollars that could be created. The rate of currency debasement was much milder compared to today.

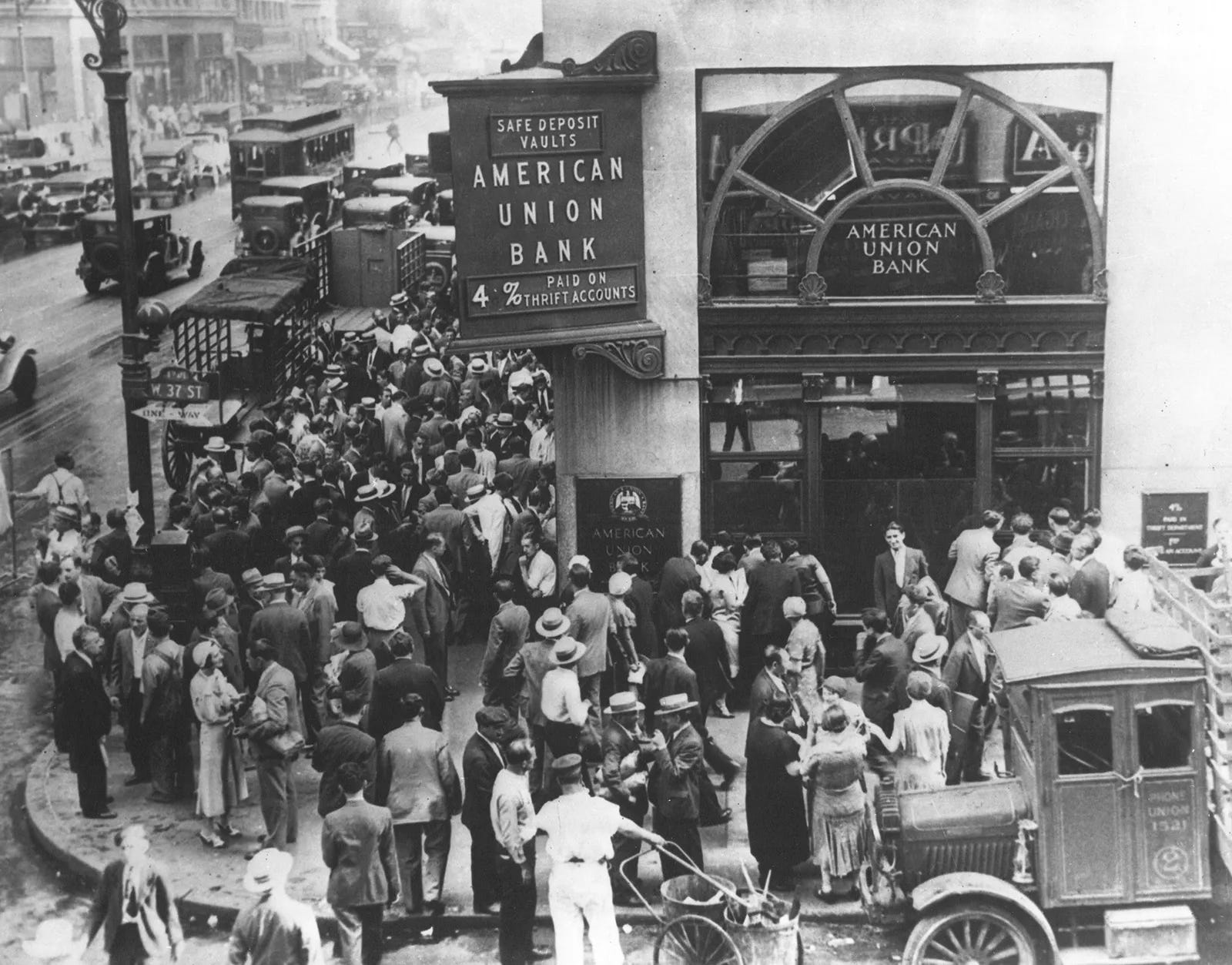

Also, these people grew up in and around the Great Depression, which dramatically influenced their mindset and worldview. At least in our relationships, these generations appeared more risk averse and conservative and unwilling to take on much risk with their savings. And again, there was less need to invest because the rate of inflation was moderate over the long term.

Baby Boomers & Generation X

Experienced the tail end of the partial gold standard and have lived primarily during the fiat standard. Compared to the previous two generations, the rate of inflation was higher, especially in the 1970s and 1980s, following the abandonment of the gold standard in 1971.

The rule of thumb savings strategy shifted to financial assets, primarily stocks and bonds. The 1970s were a great decade for hard assets. The gold price rallied from the peg of $35/oz in 1971 to $800/oz. However, the Federal Reserve's fight against inflation in the 1980s hurt precious metals prices as Federal Reserve Chairman Paul Volcker raised interest rates to a peak of 20% in 1981.

Since then, interest rates have been in a secular decline, which has benefitted asset prices broadly. Interest rates declined from 20% to 0% for the first time during the Great Financial Crisis. The combination of technology, strong demographics, and globalization created a low inflation environment, which allowed for interest rates to march lower from their highs in the 1980s.

Of course, in addition to that, the Fed would lower interest rates, and the government would add more debt in each crisis. The legitimate drivers of lower rates paired with the intervention by central banks and created an attractive environment for assets over those four decades. The "60/40 Portfolio," comprised of 60% equities and 40% bonds, became the "rule of thumb."

Millennials & Generation Z

These generations have only lived during the fiat standard. A small percentage of this demographic even knows what "fiat currency" is, and there are still many people who think we are on a gold standard.

At any rate, these generations have adopted similar approaches as the Baby Boomers & Generation X; however, the passive investing trend became a popular "rule of thumb" in the past two decades. Exchange Traded Funds (ETFs) such as SPY, which tracks the S&P 500, have become a standard approach to saving money. Overall, it became even more accessible to "save" through these financial products in the past two decades.

The older millennials who lived through the Great Financial Crisis and understood what happened became disenfranchised by the corrupt financial system and discovered bitcoin shortly after its launch in 2009.

The invention of bitcoin is the key differentiator between these generations and the ones that came before it. Those who see the benefits of decentralized digital hard money have embraced it, yet that is still a small portion of the generations.

For the most part, there have not been many differences so far between this segment of generations and the previous, aside from buying financial products at higher valuations due to the lower interest rates. Generation Z has embraced passive investing and the "crypto" ecosystem, which is largely unregistered securities or outright scams.

We will note as well that across all these generations, home ownership has been a cornerstone in building wealth and a key tenet of the "American Dream."

{kind=link}

However, home ownership has become increasingly out of reach, in part because of the dynamic written in today's article, and that is, people are looking to put their savings somewhere, which has driven up the price of homes.

In addition, home values have been supported by decades of lower interest rates, and remember, it's not the home becoming more valuable. It's the currency becoming worth less.

Homeownership definitely has been a "rule of thumb" for savings and wealth creation.

As we will explore more in part two of this series, there are major shifts underway at the macro, political, and geopolitical levels, which will influence the "rule of thumb" for managing one's savings going forward.

Based on the research we have done, we expect these developments to be positive for bitcoin adoption, resulting in it becoming the next "rule of thumb."